Mandatory Reporting on ESG

in Compliance with the ESRS Standard

Leverage Expert Knowledgein Compliance with the ESRS Standard

In accordance with the CSRD directive, which came into effect on January 5, 2023, all large enterprises and publicly listed companies (excluding micro-enterprises) will be required to disclose information regarding the impact of their activities on people and the environment. The first reports under the new regulations must be published in 2025, encompassing data from the 2024 fiscal year. The introduction of the ESRS aims to standardize reporting practices, facilitating data comparison among organizations and providing greater transparency for investors and other stakeholders.

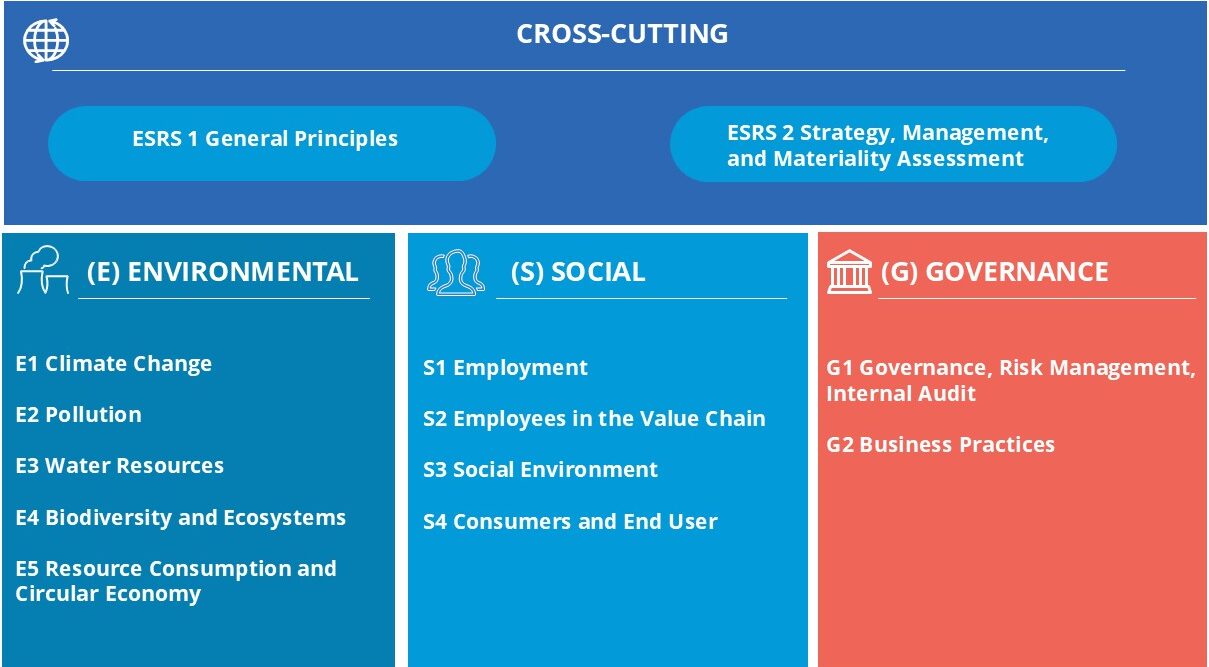

Overview of ESRS:

Main ESRS Categories:

Category E (Environmental)

The environmental category focuses on disclosing information regarding the company’s impact on the natural environment. Within this category, companies are required to report on:

- Greenhouse gas emissions and climate change management

- Use of natural resources, including water and energy

- Impact on biodiversity and ecosystem protection

- Waste production and management

Category S (Social)

The social category encompasses aspects related to corporate social responsibility, including:

- Human rights and working conditions

- Gender equality and workplace diversity

- Employee safety and health

- Impact on local communities and their development

- Consumer issues, including product and service safety

Category G (Governance)

- The governance category focuses on disclosing information regarding:

- Management structure and governance practices

- Anti-corruption policies and anti-money laundering measures

- Roles and composition of company bodies concerning sustainability

- ESG due diligence procedures

- Risk management and identification of areas significant for sustainability